Multipass is a financial services provider offering global business accounts, multi-currency payments, and cross-border transaction solutions.

Read case studyLaunch Your Own Branded Wallet

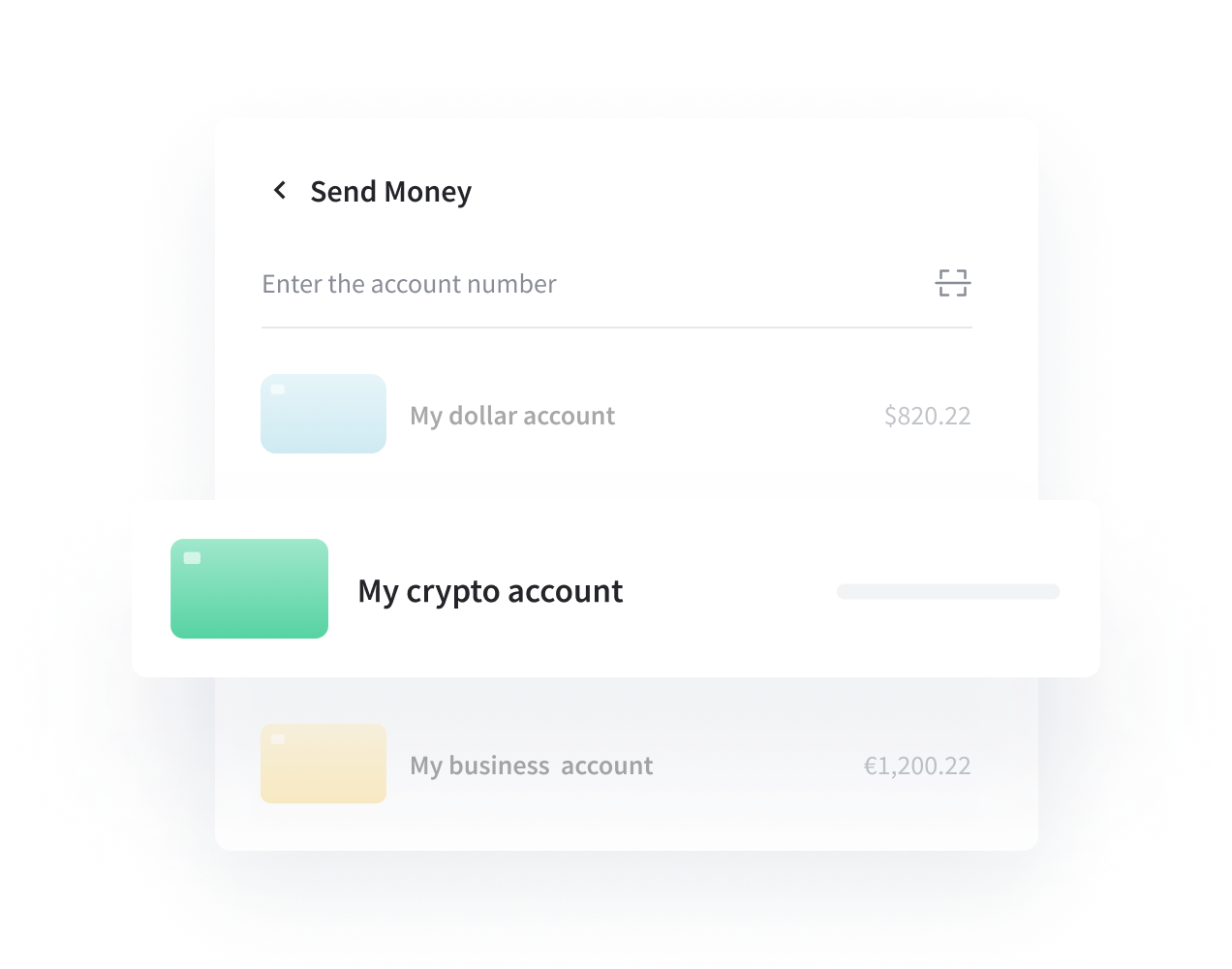

Give customers a wallet to hold money, pay and get paid: balances and IBANs, instant P2P transfers, cards with Apple Pay and Google Pay, currency exchange and top-ups. Closed, semi-closed or open-loop - one platform runs all three, live in weeks.

- Balances and IBANs

- Instant P2P transfers

- Currency exchange

- Apple Pay and Google Pay

- Top-ups and payouts

Case Studies

Paysend & Crassula - a banking solution for international companies

Read case studyLuxPay is at the forefront of providing advanced financial services, designed to meet the needs of modern businesses and consumers alike.

Read case studyWickie offers secure and scalable fiat and cryptocurrency payment solutions, providing users with digital wallets and seamless financial services across multiple platforms.

Read case studyClosed, semi-closed or open-loop? Start with the right one

The loop model decides your licensing, your acceptance reach and your economics. Picking wrong in year one is expensive. Here is the quick version, and Crassula runs all three, so you can graduate from one to the next without rebuilding.

Closed-loop

Spend within your brand

Stored value usable inside your ecosystem: gift balances, in-app credit, loyalty. Lightest to launch, often outside heavy licensing.

Semi-closed

A network of merchants plus P2P

Spend across accepting merchants and send money peer to peer. The model behind most consumer wallets. Usually needs an EMI or an agent arrangement.

Open-loop

Spend anywhere cards work

Full acceptance through card rails and bank transfers, with your own IBANs and cards. The route to competing with the big wallets.

Everything customers expect in a wallet

Balances and IBANs

Multi-currency balances with dedicated or virtual IBANs for top-up and withdrawal.

Instant P2P

Send and request money by phone number or username, split bills and share payment links, the features that make a wallet spread.

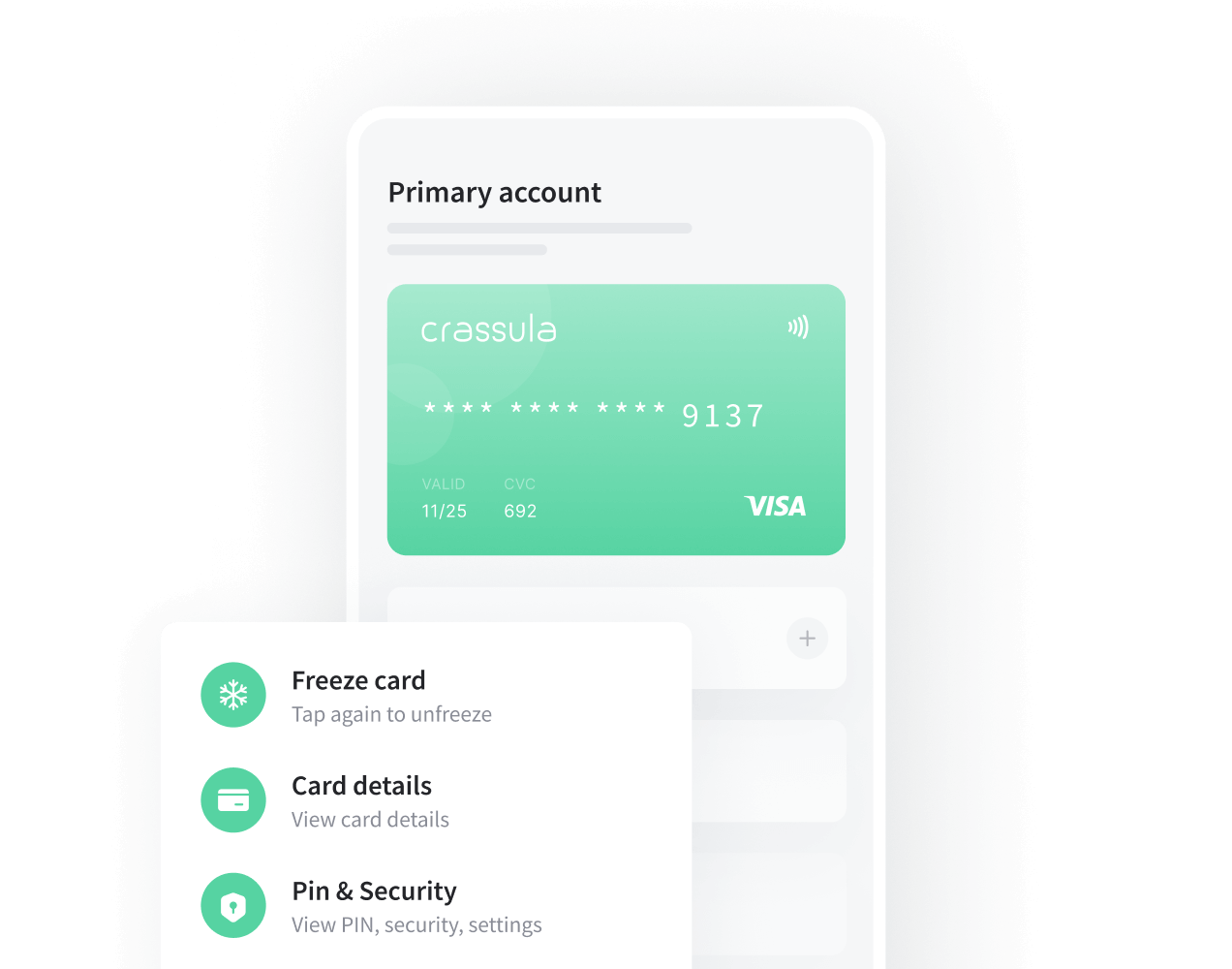

Cards in the wallet

Virtual cards on signup and physical cards on request, provisioned into Apple Pay and Google Pay.

Exchange and top-ups

Currency exchange inside the wallet, QR payments in store, plus top-ups and withdrawals by card and bank transfer.

Push and engagement

Real-time push notifications keep customers in the app, which is where wallet retention is won or lost.

KYC and controls

Onboarding, KYC and transaction monitoring you operate, with a Back-Office Dashboard to run the program.

See it in the wallet

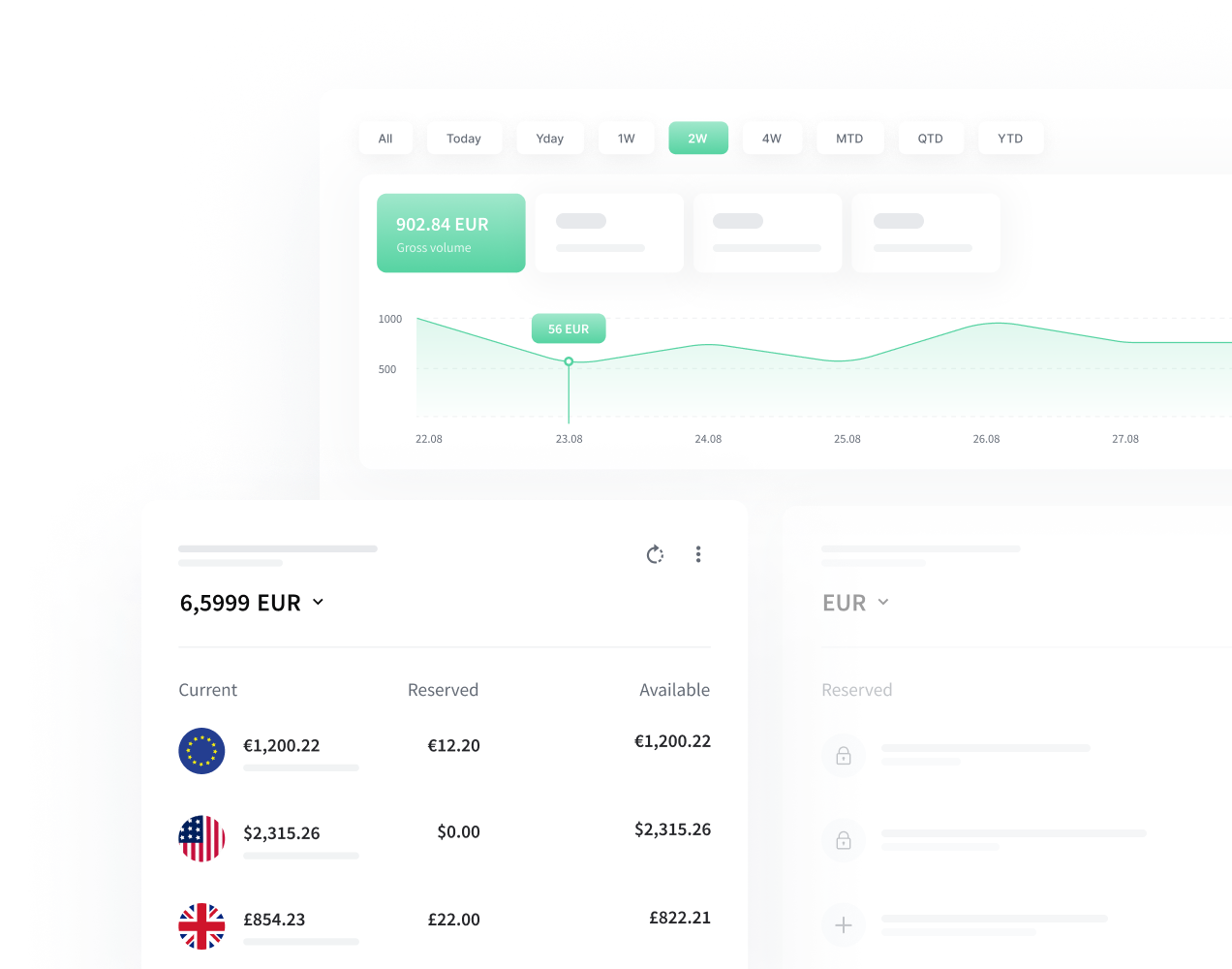

One balance, many currencies

Customers hold several currencies in the same wallet, each with its own dedicated or virtual IBAN so top-ups and incoming payments land on the right balance automatically.

Dedicated and virtual IBANs for top-up and withdrawal

Dedicated and virtual IBANs for top-up and withdrawal- Reserved and available amounts on every balance

- Closed, semi-closed or open-loop, on one platform

P2P is your growth engine

Every time a customer sends money to someone who does not have your wallet yet, that is an invitation to join. Instant transfers by phone number, payment requests and split bills turn your users into your acquisition channel, and push notifications bring them back.

A card in the wallet, in Apple Pay and Google Pay

Give customers a virtual card the moment they sign up and a physical card on request, provisioned into Apple Pay and Google Pay. They can freeze the card, see details or set limits straight from the app.

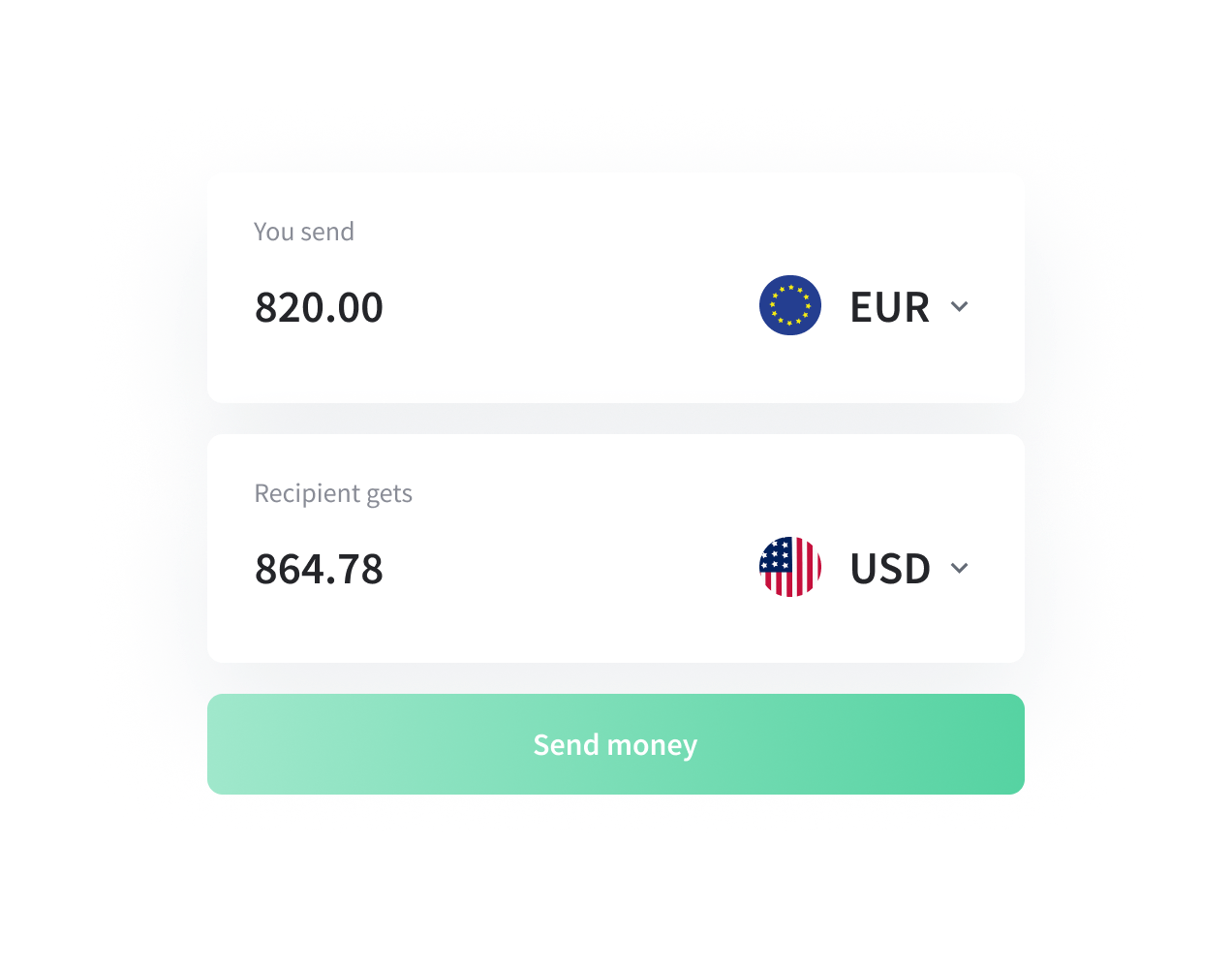

Exchange, top up and get paid

Swap between currencies inside the wallet at a clear rate, top up by card or bank transfer, and cash out to an IBAN. QR payments in store round out the day-to-day spending customers expect.

Wallets that pay off

Retail and loyalty

A closed or semi-closed wallet with stored value and rewards keeps spend inside your brand and lifts repeat purchase.

Keep spend in your brand

Marketplaces

Hold buyer balances, pay out to sellers and move money inside the platform without slow bank transfers.

Instant on-platform payouts

Gig and payouts

Pay workers into an instant wallet with a card, so earnings are spendable the moment a job clears.

Earnings spendable at once

Super apps and communities

Add money movement to an app people already open daily, and let payments deepen the habit.

Payments inside the daily app

3

loop models: closed, semi-closed, open

Weeks

to a live branded wallet

150+

companies run on Crassula

15+

languages out of the box

Wallets, explained

FAQ

Closed-loop wallets spend only within your own brand. Semi-closed wallets spend across a network of accepting merchants and support P2P. Open-loop wallets spend anywhere card networks are accepted. Each model has different licensing and acceptance - Crassula runs all three, so you can start light and graduate.

It depends on the model. A closed-loop wallet often sits outside heavy licensing; semi-closed and open-loop wallets that hold spendable funds usually need an EMI licence or an agent arrangement. You can launch on a partner and bring your own licence later - Crassula supports both.

Yes. Instant P2P transfers by phone number or username, payment requests and split bills, plus QR payments, top-ups and withdrawals are all built in, along with virtual and physical cards.

A wallet is a lighter product focused on holding value, paying and P2P - often ideal for retail, marketplaces and loyalty. A digital bank is the fuller stack with accounts, lending and broader banking. Crassula powers both; many brands start with a wallet and expand. Digital banking solution.

A branded wallet on ready-to-market apps launches in weeks. The main variable is your licensing or partner setup, not the Crassula build.