An Ultimate Guide To Digital Banking: What Is It And How It Works?

Digital banking is a one-in-a-lifetime opportunity that offers numerous advantages and ways to improve your business.

Contrary to popular belief, digital banking is not a recent innovation like blockchain and crypto. It's a financial breakthrough that was introduced nearly 30 years ago and continues to be a preferred choice for businesses and customers worldwide.

However, it is still not a rare case when people wonder, "What is digital banking?". If you belong to this category, the guide on this page will certainly be useful for you, especially if you own or run a business. You will receive an exhaustive explanation of how digital banking works, its features and types, and a quick guide to its advantages and disadvantages.

What is digital banking?

Contrary to popular belief, digital banking is not a recent innovation like blockchain and crypto. It's a financial breakthrough that was introduced nearly 30 years ago and continues to be a preferred choice for businesses and customers worldwide.

However, it is still not a rare case when people wonder, "What is digital banking?". If you belong to this category, the guide on this page will certainly be useful for you, especially if you own or run a business. You will receive an exhaustive explanation of how digital banking works, its features and types, and a quick guide to its advantages and disadvantages..

Let's discuss your project and see how we can launch your digital banking product together

Request demoWhat Is Digital Banking

Digital banking is a modern financial solution that enables customers and businesses to conduct transactions online. It's essentially any service that facilitates financial operations via the Internet. While the term "banking" is used, these services are "not exclusive to banks. They can be offered by any fintech business involved in money and payments.

The efficiency provided by the digital banking system contributed to its rapid growth and development. Therefore, we can take advantage of it in hundreds of markets and in dozens of ways.

It's no surprise that digital banking's Net Interest Income increases each year. According to Statista's analysis and forecast, this tendency will continue in the next five years and will be even more striking. Thus, the income from digital banking is expected to increase by more than 100% by 2028.

Digital Banks And Traditional Banks: How They Differ

Still, efficiency and convenience are not the only specific features of digital banking solutions that make it different from traditional banks. Indeed, digital and traditional banks are not the same. They are interconnected but not equal. Thus, you can expect to see the services offered in traditional banks in digital banks as well. At the same time, traditional banks have adapted to the new reality and partially offer digital banking services.

Let’s take a look at the main features that let you differentiate those two services:- The way an account is opened: with digital banks, the account opening is made online, while you often need to show up in person to open an account at brick-and-mortar banks.

- Accessibility: All digital banking services are available 24/7, while there are operating hours in brick-and-mortar banks.

- ATMs: Digital banks do not have ATMs, so money withdrawals can be made in partner banks, and an extra fee is applied. Traditional banks have a wide network of ATMs.

- Cost: Digital banks offer lower costs and charges compared to traditional financial institutions.

Digital Banking Vs. Online Banking Vs. Mobile Banking

This guide would not be complete without explaining the difference between digital, online, and mobile banking. Surprisingly, even those experienced in fintech operations are often confused about those three categories.

Digital banking is an independent service that offers a full range of financial solutions to businesses and individual customers. All operations are conducted online and 24/7, so there are no time limitations for customers. Moreover, those who use digital banking products benefit from high cost-efficiency, security, and flexibility.

Online banking is far more limited than the abovementioned category, as it usually includes a series of online services that traditional banks offer to their customers. Those are some payments and operations that can be conducted via the Internet, so that account holders do not need to go to the brick-and-mortar bank.

Online and mobile banking are quite similar, as they share practically the same list of services. The main difference between them is that online banking can be done in a web browser, while mobile banking is designed for mobile devices. Thus, mobile banking usually includes specialized Android and iOS apps released by banks.

Who Offers Digital Banking Solutions?

As you might have already understood from the information above, there are different institutions that offer digital banking services. They differ slightly from market to market but can be classified into two major categories: traditional banks and online financial institutions.

Traditional Banks

For traditional banks, the function of digital banking is quite obvious. To ensure convenience for their account holders, banks transfer some of their services online to give their customers a chance to make payments, money transfers, and more without leaving their homes. Furthermore, this innovation makes banking more flexible for customers.Online Financial Institutions

This category is quite extended, and it includes all the financial institutions that provide payment services and do not have physical branches. Those might be e-wallets, credit associations, exchanges, etc. The selection and availability of such online financial institutions depends on the market.Types Of Digital Banks

Given the range of services online financial institutions provide and how those services are strongly associated with the banking system, it is no wonder they are called digital banks. Experts divide them into three major categories. Each digital banking platform listed below has specific features that make it stand out from others.Neobank

Neobanks are companies that are less associated with banks and more with startups. Indeed, they are striving for innovation and have a clear goal of having as big a customer base as possible. They are not regulated as banks, so their services and policies are far more flexible. A wide range of services offered by neobanks are similar to those of traditional banks. Thus, their customers can make payments quickly and have a debit card issued for convenience. A user-friendly mobile app is also a must for a neobank. At the same time, loans are not often listed among the provided services. Those are more of an exception than the rule. Overdrafts and deposit protection (which are valued by customers of traditional banks) are not available at neobanks. At the same time, omnichannel experience and advanced chatbots are common attributes of this type of digital bank.Challenger Bank

Out of all types of digital banking, challengers are the most similar to traditional banks. They are even regulated similarly and offer a range of services that is most similar to brick-and-mortar financial institutions. Their main goal is to grow the balance sheet. In contrast to neobanks, challengers do offer loans and deposit protection to their customers. Moreover, overdrafts are possible. Therefore, this type of financial service is often called branchless banking.Nonbank

Out of the three types discussed in our article, nonbanks are the most distant from the banking system, as they provide only some of the services that are typical for banks. Thus, the list of nonbanks includes mortgage providers, P2P borrowers, loan associations, insurance companies, etc. They are less regulated and, as a result, less secure. Nonetheless, such destinations are popular with customers and businesses that are not able to receive certain services in banks.Range Of Digital Banking Services

One of the main benefits of digital banking is the range of services it offers. That flexibility in terms of options is one of the main reasons why this type of financial service is flourishing currently and has such big potential in the future. Some of the services are commonly known, while only industry experts are aware of others. Regardless of whether you are new or experienced in financial matters, you will find it useful to explore each of the most popular digital banking services listed below.Card Payments

Card payments are one of the most widespread services offered by digital banks. Even if you are not a fintech expert, you have certainly taken advantage of card payments that make all the payments much more efficient. Cards can be credit and debit ones, but their main functions remain the same. These are goods purchasing, payment for services (especially online ones), payment of utility bills, fulfillment of business money transfers, etc. It is also worth noting that digital cards are widely used in digital banking. They have high cyber security, which makes them safe for use on the Internet, as the risks of fraud are much lower.Digital Wallets

Also known as electronic wallets, digital wallets are a good alternative to traditional banking. They can often be used as mediators between banks and different businesses, allowing you to make payments and transactions without disclosing your financial details to third parties. These fintech solutions work in the following way: you create an account on the website (or mobile app), top up the balance with your bank card, and make payments wherever you need. Often, digital wallets have an option of card issuing to make payment processes similar to those of traditional banking.Internet Banking

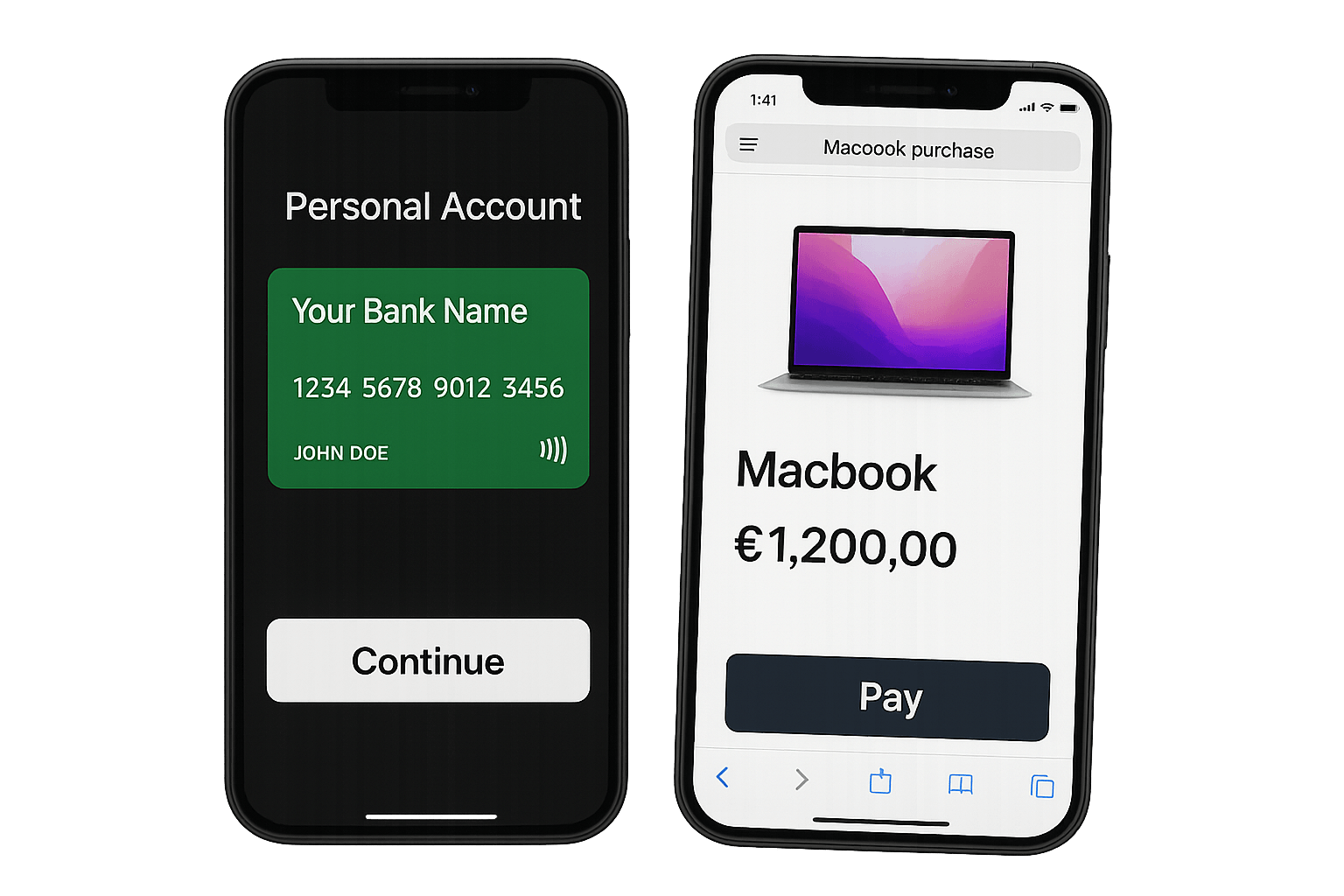

This service is a perfect example of digitalization in banking, as here, you can receive practically all the same services as in brick-and-mortar banks. The only difference is that everything is made online. This means you do not need to spend time and money commuting to the bank to make payments or other financial activities. Checking your bank statement is also possible through Internet banking.Mobile Banking

With the evolution of smartphones, the appearance of mobile banking was inevitable. Those familiar with Internet banking will not be surprised by the functionality of this type of digital banking service, as practically all the possibilities were preserved and transferred to smartphones. Enhanced security is certainly a benefit of mobile banking over Internet banking, as customers can use biometric authentication. This type of banking also makes shopping much easier as contactless payments are possible thanks to NFC technology and Google Pay and Apple Pay services.BaaS

BaaS (meaning Banking as a Service) is an innovation that is currently growing in popularity across different markets, overcoming traditional banking services. Thanks to these solutions, different financial institutions can connect with banks via APIs and build their services on already existing infrastructure. Digital banking development with the BaaS process is much more cost and time-effective. Thus, many new fintech businesses select it instead of traditional banking, revolutionizing the way the financial industry works.Embedded Banking

Some users do not even suspect that many examples of digital banking have this service behind them. Embedded banking allows different business and financial institutions to offer payments and other financial solutions without building their own banking instructions. They can cooperate with banks to provide some services to customers and benefit from the cost-saving efficiency offered by embedded banking. This banking innovation is secure and commonly used and end customers might not even suspect that it is in place. Buy Now Pay Later (BNPL) and Credit Reporting are just some of the examples of embedded finance.Cloud-Native Banking

While this type of digital banking seems to be the same as other services to the end customer, it stands out significantly from all those described above. The main difference is in how the database and information about transactions are stored. As you might have guessed from the name, all the information is hosted on the cloud. Artificial intelligence (AI) and machine learning technologies are used to ensure the proper functioning of this service.Cloud-native banking is faster and smoother than other digital banking services, so it offers a wide range of possibilities to those businesses that implement it.

Pros And Cons Of Using Digital Banking Platforms

Now that you are no longer puzzled by the question, "How does digital banking work?" Let's examine the advantages and disadvantages of this innovative financial solution.

Among pros, the following aspects can be listed:- Access: In our digitalized world, having payment services available 24/7 is highly valued. Therefore, being able to make payments at any time on mobile and desktop devices is a big plus.

- Lower fees: Since digital banking is much cheaper than traditional banking, providers of those services have more flexibility in terms of customer charging, so fees are often much lower.

- Equity: Online banking makes banking services more accessible, as communities that haven't had access to banks in their area can now create an account and enjoy the financial benefits.

- Downtime: Any online service might experience an outage at some point, so customers who rely only on digital banking will be deprived of the possibility of making payments and transfers.

- Background needed: it might be challenging for those not tech-skilled to use online banking.

- Security: While security measures in digital banking are still good, traditional brick-and-mortar institutions have more sophisticated security measures in place, which are tested over time.

Digital Banking Industry Outlook

Given the rapid development of technologies, financial industry experts consider digital banking to evolve with time and offer even more progressive solutions to customers. They also predict the increasing popularity of online financial services and expect them to overtake traditional solutions in the near future.

Currently, almost half of account holders opt for mobile banking as their first option, and this percentage will increase in upcoming years as digital banking adapts to a new reality quicker than a traditional one. We might also expect even more innovative ways of payment than they are now. For example, biometrics might be implemented to pay in grocery stores, so being able to make a transaction with your finger and not even your phone might become a reality.